服装行业谁有办法清库存,谁就有实力进一步走下去

【YKK拉链行业新闻】在过去几年里,饱受打击的服装和零售行业也失去了很多地位,但自2017年以来,降温形势有所改善。

在线渠道在其中起到了一定作用,唯品会的崛起表明,库存销售是一项不错的业务:

服装是高频的,只需要一半的标准产品,有广阔的市场;

服装种类不可能缺货。由于季节性和时尚性的原因,货物的滞销意味着储存利息和过期的风险。

服装产品的增长率一般是2倍以上,毛利率高,使平台有足够的差价来支持打折特价销售和利润。

唯品会特价销售模式收取扣除点利润,可以坚持毛利率相对稳定,20%~25%,嘉兴ykk拉链但稳定性是好事,也是极限。特殊的销售模式需要继续稳定交通,与快速的物流系统合作。由于在线客户利率越来越高,唯品会的利润空间越来越小。

2017年,唯品会开始撕下库存特价标签,打破模式的天花板,转型为“全球精选、正宗特卖”的另一个主要渠道,天猫开始将重点转向食品保健。

这给了新球员一个机会。社交电子商务公司如群集、全球捕手和pedodo的奇迹指出了社交网络的价格低迷,两个公司在微信上进行库存分配,在月中筹集资金。

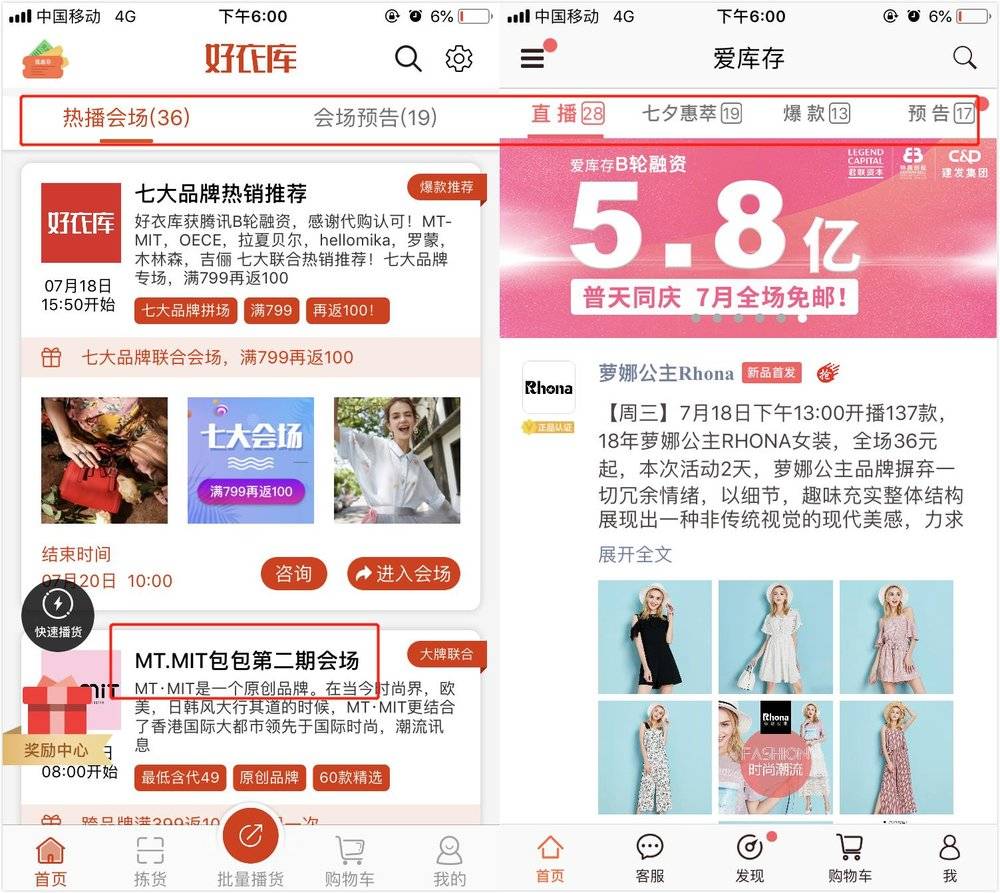

7月2日,aidsu完成了由junlian capital牵头的B轮融资5.8亿元,其次是中鼎风险投资和中国发展集团。

7月17日,优衣库完成了由腾讯领导的数亿元人民币b轮融资,紧随其后的是IDG风险投资集团长青和袁静。充盈资本作为这轮融资的独家财务顾问。就在今年6月,优衣库宣布,以IDG capital为首的一轮融资规模为1亿元人民币。

平台的应用形式,两家公司几乎没有区别:S2b2C模型,上游与品牌的库存方面,下游为专业提供真正的和低价库存wechat代理商购买,产品由wechat分布式业务,形成一个新的交易系统对消费者品牌的一面——平台——小乙wechat购买代表品牌。

简而言之,这两家公司是低发行版的唯品会+。

限时库存销售,低发行版“唯品会”

好衣服和爱的库存定位是明确的,就是在做网店前做些什么:库存销售。

根据这两个app的内容,我们还可以看到大家熟悉的“提前通知”和“截止订单”,台州ykk拉链我们可以判断服装仓库和love inventory与唯品会的销售模式相似。

会议地点的销售日程和预览与唯品会类似

谈一谈第一只产品将销售模式:品牌第一次宣布他们的唯一产品预测,预测销售货物发送货物到仓库后,库存,开始的时候活动,品牌方在后台检查销售情况,定时减少单,每一个部分,只有产品仓库交货,客户返回返回到品牌方仓库直接将返回剩余的货物后本赛季。

模式Vipshop出售没有租用成本,但扣点高约为30%,但Vipshop迅速处理大量的库存商品,温州ykk拉链和更少的价格影响其他在线或离线品牌系统(Vipshop和淘宝商城,京东用户重叠程度不高)国内外一二线品牌Vipshop清理库存,甚至一些品牌将Vipshop作为主要的销售渠道,加速现金流。

好的服装店和爱心库存的上游也与品牌库存相联系,但它是一个低分销的版本。与唯品会相比,好衣库的品牌定位较低,库存较少,工作时间只有3天。此外,从特价销售品牌的角度来看,服装仓库明显比唯品会低一到两个层次。另外,根据宜博的报告

Over the past few years, the battered clothing and retail sectors have also lost much of their status, but the cooling situation has improved since 2017.

According to the analysis of changjiang securities, the wholesale destocking at the level of China's textile and clothing industry was basically completed in 2016, and the channel destocking at the same time was approaching the end. The overall performance of China's garment sector began to improve in 2017, mainly due to the digestion of inventory. This is also in line with the industry's argument that the industry depends on who makes money, and whose inventories are cleaner.

Online channels play a part in this, and the rise of Vipshop shows that inventory sales are a good business:

Clothing is high frequency, just needed half standard products, there is a broad market;

It is impossible for the clothing category to be out of stock. Due to the seasonal and fashion nature, the late sale of goods means the storage interest and the risk of being out of date.

The increase rate of clothing products is generally more than 2 times, and the gross profit is high, which enables the platform to have enough price difference to support the discount special sale and profit.

Vipshop special sales mode charges the deduction point profit, can insist the gross profit rate is relatively stable, 20%~25%, but stability is a good thing, but also a limit. The special selling mode needs to continue to stabilize the flow of traffic and cooperate with the rapid logistics system. As the online customer interest rate is higher and higher, Vipshop's profit space is lower and lower.

In 2017, Vipshop began to tear off the inventory special sale label, break the ceiling of the mode and transform into another major channel of "global select, authentic special sale", while Tmall began to shift its focus to food health care.

This gives new players a chance. Social e-commerce firms such as swarming, global catcher and the miracle of pedodo point to the price depressions in social traffic, with two companies doing inventory distribution on WeChat raising money in the middle of the month.

On July 2, aidsu completed a series B financing round of 580 million RMB, led by junlian capital,ykk拉链followed by zhong ding venture capital and China development group.

On July 17, uniqlo completed hundreds of millions of RMB b-round financing, led by tencent, followed by IDG venture capital group changqing and yuan jing. Chong ying capital acted as the exclusive financial adviser for this round of financing. Just in June, uniqlo announced A rmb100m a-round led by IDG capital.

From the platform of App form, there is little difference between the two companies: the S2b2C model, the upstream connects with the inventory of the brand side, the downstream provides the genuine and low-price inventory for the professional wechat business agent purchase, and the product is distributed by wechat business, forming a new trading system for consumers of the brand side -- platform -- small b WeChat purchase on behalf of the brand side.

In a nutshell, these two companies are the low-distribution version of Vipshop +.

Limited time period inventory sales, low distribution version "Vipshop

Good clothes and love inventory positioning is clear, is to do Vipshop before doing something: inventory sales.

According to the content of the two apps, we can also see the familiar words of "advance notice" and "cut-off order", and we can judge that the clothing warehouse and love inventory are similar to Vipshop's selling mode.

The selling schedule and the preview of the meeting place are similar to Vipshop

Talk briefly first only product will sale mode: brand first to declare them in the only product for forecast, forecast sales after the goods sent to goods to warehouse, inventory, at the start of the activity, brand square in the background check sales situation, timing cut single, every section, only products are a warehouse delivery, customer return is returned to the brand party warehouse directly, will return the remaining goods after the season only.

Mode Vipshop sale without occupancy costs, but buckle point is high at about 30%, but Vipshop quickly dispose of a large number of inventory goods, and less impact on the price of other online or offline brand system (Vipshop and Tmall, jingdong users overlap degree is not high) at home and abroad by a second-tier brands Vipshop clearing inventory, or even a few brands will Vipshop as the primary sales channel, accelerate cash flow.

The upstream of good clothes store and love inventory also connect with the brand inventory, but it is a low distribution version. "compared with Vipshop, good clothes warehouse locates low line brands and shallow inventory, with a small amount of work schedule only for 3 days. Moreover, from the point of view of the special selling brands, the clothing warehouse is obviously one or two levels lower than Vipshop. In addition, according to the report of yibo power, most orders on the platform of the clothing warehouse are directly delivered by the brand to the daigou or consumers.

From the perspective of business connection only, for the brand side, there is no difference between the special sales of good clothes warehouse and love inventory and the special sales of Vipshop, which means that the brand side will encounter the same problem in good clothes warehouse and love inventory.

On the one hand, the discount will have an impact on the brand image. The more important model of special sales has not stabilized the store and user evaluation. Therefore, the online brand building position is generally able to face the consumers' Tmall and taobao.

But only has one batch of products meeting by continue to sale of the brand, often on taobao, Tmall survival difficult, presumably good library and love on the inventory may also have this kind of phenomenon, but you can be sure if anyone has the potential to do big, without the brand sale is willing to do for a living, and it is WeChat this hidden, do not brand awareness.

Wechat business distribution consumer upgrade"

There are several main ways to play social traffic on WeChat: haggling prices, scrabbling, head-pulling and distribution. WeChat's relationship chain is naturally suitable for distribution mode.

Take a case study. On May 11, 2018, at the third anniversary celebration, Mr. Xiao announced that the annual GMV of his platform will exceed 10 billion yuan in 2017, with 4 million merchants and more than 3 million shopkeepers (i.e. paying members). Although there is no more third-level distribution, even first-level distribution will give shopkeepers a chance to earn a profit.

Like huazhong, good clothes store and love inventory are also S2b2C models "and distribution is also the main social game.

Good clothes storehouse, love stock also needs invite code ability to use, good clothes storehouse does not collect member charge, love storehouse should pay 298 yuan membership fee, sell inside two months full 5000 yuan returns. The membership fee of 298 yuan is the same as that of zhonghu. After paying 398 yuan platform service fee, zhonghu will become the owner. At the heart of both is screening "traffic entry" shop owners.

Increasing the entry threshold, on the one hand, is to screen accurate users, on the other hand, is also to raise the threshold of the platform. If there is no hierarchical differentiation, then distribution cannot play a role.

In addition, the profit of clothing is not as high as that of cosmetics and health care products. Therefore, although the clothing warehouse and love inventory are "low-quality", they are far more "compliant" than those gathered at wechat business.

However, without the "off-line" commission mechanism, both uniqlo and aiqlo lack the driving force of "sharing and making money". They can only rely on price driven.

As a platform party, uniqlo and aiqlo can charge certain deduction points to the brand party, or directly buy out self-management to improve profits. For wechat business, the platform provides a channel for them to get authentic goods at low prices, and should provide assistance and incentive as far as possible so that they can distribute more brand inventory.

In the end, the birth of Vipshop + of "low distribution" Vipshop +, the "low distribution" Vipshop +, and the advantage of flow price, let wechat business come to the surface before "low and not guaranteed", the so-called "efficient brand to inventory, daigou stand to earn money, consumers good goods are not expensive" or not expensive "on the key.

- 上一篇:光影团队对于时装秀起到决定性作用 2018/7/23

- 下一篇:时尚行业开始接受哺乳期的母亲 2018/7/22